Guide To VAT Domestic Reverse Charge

HMRC introduced the VAT domestic reverse charge procedure that shifts VAT liability from the supplier to the customer.

These rules affect companies that operate within the Construction Industry Scheme (CIS) (with a few exceptions that we’ll detail later on) and have an impact on VAT compliance, as well as cash flow.

By introducing these rules HMRC hopes to reduce ‘missing trader’ fraud, which occurs when a company sets up a construction business, charges VAT to customers and disappears (ceases trading) before tax is due, effectively pocketing money that doesn’t belong to them.

It’s estimated that tackling this VAT fraud will raise over £100 million a year.

Key Points

The key things to remember when using the reverse charge are:

• Only VAT-registered businesses supplying and receiving CIS regulated services are eligible

• It only applies to work that is subject to VAT at 5% or 20%. It doesn’t apply to work that is zero-rated or subject to VAT exemption.

• The business receiving the service (the customer) is responsible for paying the VAT

• VAT invoices must make it clear that the customer has to make a reverse charge entry

• It applies to all projects completed on or after 1 March 2021

What is the VAT domestic reverse charge?

To explain how the VAT domestic reverse charge works, it helps to briefly explain how VAT typically works.

As a VAT-registered business operating in the UK, you add the UK rate of VAT to your taxable sales, which is passed on to the customer. The customer pays the VAT as part of their invoice and you pay what this to HMRC on your VAT return.

You also get to reclaim the VAT you pay to other businesses on taxable purchases (as long as they are not VAT exempt or out of the scope of VAT).

With the VAT domestic reverse charge, rather than you collecting the VAT from the customer and paying it to HMRC on their behalf, the customer pays it directly to the government themselves. They may then recover the VAT amount as input tax, subject to the normal rules.

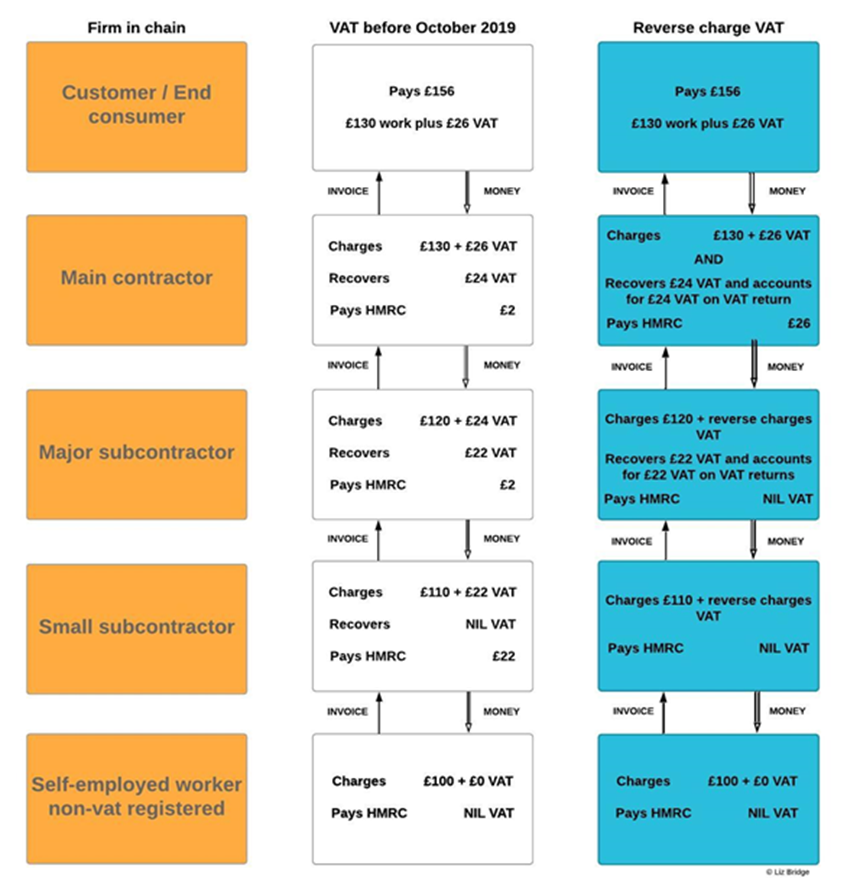

Here is an example of how the reverse charge works in practice.

Subcontractor Stuart is hired by Contractor Colin for building work that costs £3,000+£600 VAT. This work is a business-to-business (builder-to-builder) supply so it falls under the reverse charge rule (more on these rules shortly).

Under the current (non-reverse charge) rules, Stuart invoices Colin for £3,600 & includes the £600 on his VAT return as output tax in box 1.

Colin then claims input tax of £600 in box 4 of his VAT return and records the next expenditure of £3,000 in box 7.

Under the reverse charge rule, Stuart instead invoices Colin for £3,000 and doesn’t include the £600 VAT. Instead, he adds a note that states Colin must deal with the VAT on his VAT return using the reverse charge.

Now, Colin has to enter the £600 VAT in box 1 of his VAT return.

So, the only change is that Stuart’s box 1 entry has shifted to Colin’s box 1 entry. HMRC still receives the correct amount of VAT.

The following table demonstrates the old and new vat treatments for the different parties in the supply chain.

Image is copyright © Liz Bridge and The Construction Index.

Who does the VAT DRC apply to?

The VAT reverse charge applies for standard and reduced-rate VAT ‘specified services’ for VAT-registered individuals and businesses in the UK that operate within the Construction Industry Scheme (CIS).

If you’re a contractor that employs subcontractors or a subcontractor who is employed by contractors and you’re signed up to CIS, the VAT domestic reverse charge will apply to you.

Specified services are those services classed as construction operations under CIS. For example:

• Construction, alteration, repairs and demolition of building structures

• Civil engineering work

• Heating, lighting, power, water and ventilation system installations

• Prep work (e.g. site clearance, laying foundations and erecting scaffolding)

• Cleaning a site after construction work

The VAT reverse charge doesn’t apply to:

• Contractors or subcontractors whose businesses aren’t VAT-registered

• Zero-rated supplies

• Work done outside of the UK

• Employees and temporary workers your business is responsible for paying

• End-users*

• Intermediary suppliers**

*End-users are individuals or businesses who use construction services for themselves and don’t sell services as part of their business. For example:

• Developers

• Housing Associations

• Domestic customers and consumers

**Intermediaries suppliers are VAT-registered businesses that are connected or linked to an end user. For example, a landlord and their tenant or a group of connected businesses that collaborate to purchase construction services.

When to use the VAT domestic reverse charge

HMRC says that you must use the VAT DRC for the following services:

• Constructing, altering, repairing, extending, demolishing, or dismantling buildings or structures (whether permanent or not), including offshore installation services.

• Constructing, altering, repairing, extending, demolishing of any works forming, or planned to form, part of the land, including (in particular) walls, roadworks, power lines, electronic communications equipment, aircraft runways, railways, inland waterways, docks and harbours, pipelines, reservoirs, water mains, wells, sewers, industrial plant and installations for purposes of land drainage, coast protection or defence.

• Installing heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems in any building or structure.

• Internal cleaning of buildings and structures, so far as carried out in the course of their construction, alteration, repair, extension or restoration.

• Painting or decorating the inside or the external surfaces of any building or structure.

• Services which form an integral part of, or are part of the preparation or completion of the services described above – including site clearance, earth-moving, excavation, tunnelling and boring, laying of foundations, erection of scaffolding, site restoration, landscaping and the provision of roadways and other access works.

If materials are supplied and used directly in any of the above services, the reverse charge should be applied to those too.

The VAT domestic reverse charge must not be used for any of the following services when they’re supplied on their own:

• Drilling for, or extracting, oil or natural gas.

• Extracting minerals (using underground or surface working) and tunnelling, boring, or construction of underground works, for this purpose.

• Manufacturing building or engineering components or equipment, materials, plant or machinery, or delivering any of these to site.

• Manufacturing components for heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems, or delivering any of these to site.

• The professional work of architects or surveyors, or of building, engineering, interior or exterior decoration and landscape consultants.

• Making, installing and repairing artworks such as sculptures, murals and other items that are purely artistic, signwriting and erecting, installing and repairing signboards and advertisements.

• Installing seating, blinds and shutters.

• Installing security systems, including burglar alarms, closed-circuit television and public address systems.

However, some services included in the above list can become subject to VAT reverse charge in certain circumstances, which can muddy the waters. This will be the case in any of the following scenarios:

• If there is a reverse charge element in the supply chain, the whole supply becomes subject to the reverse charge. HMRC gives the following example: “A joiner constructing a staircase offsite and then installing it onsite is making a reverse charge service, even if the charge for installation is only a minor element of the overall charge.”

• If the VAT reverse charge has already been used between two parties, both parties can agree to future services on a site being subject to the reverse charge.

• If more than 5% of contracts (in value or volume) are subject to the VAT reverse charge, a contractor and subcontractor can agree to apply the charge to all contracts.

• In cases where’s there’s doubt over whether a service is subject to the VAT domestic reverse charge, the charge should be applied if the recipient is VAT-registered and payments are made within CIS.

Invoices for CIS domestic reverse charge services

If you’re supplying a service where the VAT domestic reverse charge should be used, you’ll need to make tweaks to your invoices so that they include no VAT.

A note that makes it clear that the reverse charge applies and the recipient needs to account for VAT on their VAT return. So that you meet the legal requirement, the words ‘reverse charge’ have to be used. These can be written in one of three ways:

o Reverse charge: Customer to pay VAT to HMRC

o Reverse charge: VAT Act 1994 Section 55A applies

o Reverse charge: S.55A VATA 94 applies

• Details on how much VAT is due under the reverse charge

VAT domestic reverse charge as a contractor

As a contractor purchasing services, the VAT reverse charge means that you pay VAT to HMRC directly on your VAT return instead of paying the VAT on CIS supplies to your suppliers.

This may mean a bit of a cash flow boost because VAT previously paid to subcontractors and reclaimed on a future VAT return can be netted off.

To ensure you’re paying the right amount of VAT, make sure the invoices you receive are correct (the right amount of VAT is applied and services are eligible for VAT reverse charge) and properly accounted for.

You’ll also need to ensure that all VAT and CIS registered subcontractors are aware of the VAT domestic reverse charge and how VAT liability will change. It’s a good idea to contact each subcontractor individually to update them on the new rules.

If you’re taking on a new subcontractor, you can confirm their CIS-registration using the CIS verification system. VAT numbers can be verified on the European Commission website (a similar UK-specific site is likely to be launched after the end of the Brexit withdrawal agreement) or by calling the HMRC VAT helpline.

VAT domestic reverse charge as a subcontractor

As a subcontractor, the reverse charge doesn’t make a whole lot of difference accounting wise, as you’ll simply be passing on the VAT charge you would already account for.

Where you will notice a difference is in VAT-registered customers withholding VAT for CIS supplies, which will mean any VAT you would normally hold onto before paying it to HMRC on a quarterly return can no longer be relied upon to keep cash ticking over.

Because you’ll no longer be paying VAT on your sales, but still claiming VAT on purchases, you might become a ‘repayment trader’.

This will mean you’re able to move to monthly (rather than quarterly) VAT returns to speed up any payments you’re owed. You can request to switch to monthly returns via your VAT online account, or by asking your Accountant.

Reverse charge treatment for utilities

Supplies of construction services to utility businesses are likely to be outside the scope of the reverse charge because they’re the construction, repair or alteration of the utility company’s physical assets. Therefore, although they’re CIS registered the end user exclusion will apply.

Services provided by utility businesses which do not fall within the domestic reverse charge include the:

• provision of a connection to a utility network, or diversionary works to allow the relocation of the network

• development and construction of a private network to be owned by the utility and leased or sold to the customer

• installation of a boiler (and ancillary supplies)

Exceptions to this will be when a utility company takes on the role of contractor for particular projects such as:

• constructing, repairing or maintaining a private power or gas network for a customer

• installing full heating systems

Get in touch

Please contact one of the team for further information on any of these areas.

Phone: 01508 333040

Email: office@abcabacus.co.uk

Website: abcabacus.co.uk